2023 Health Savings Account

Participating in a Health Savings Account is a way of putting money aside tax-free throughout the year, and then later using those pre-tax dollars to pay for your health care that isn't covered by health insurance.

Contact Fidelity

800-544-3716

https://www.fidelity.com/

https://netbenefits.com/

Create an Account

When you enroll in a High Deductible Health Plan with the Health Savings Account (HSA) option, you will receive an email from Human.Resources.Benefits@Dartmouth.edu within a few weeks after enrollment, providing step-by-step instructions on how to set up your HSA account through Fidelity. It is important to make sure that you set up this account timely. Your and Dartmouth's contributions will not be able to upload funds into your account until the account has been established. If you elect the HDHP with HSA plan during the annual Open Enrollment period, it may take up to a month before you receive this email, but please watch your email carefully.

Eligibility and Enrollment

All benefits-eligible Faculty, Exempt, Non-Exempt, SEIU and RAB employees should check the list below carefully before enrolling in the HSA option to see if you are eligible to participate. Per IRS guidelines, you are eligible to participate if you are:

- NOT a Research Fellow or a J-VISA holder.

- NOT enrolled in Medicare, Medicaid, Tricare or any other type health insurance that is not a qualified HDHP.

- NOT a patient of Dartmouth Health Connect.

- NOT being claimed as a dependent on another person's tax return.

- NOT eligible to receive medical-expense reimbursement under your own general-purpose Health Care Flexible Spending Account (HCFSA) or that of a spouse or a parent.

The above IRS governed rules apply only while contributing to or receiving employer contributions to your HSA account.

If you have a balance in your HSA account at year end and switch medical plans or leave Dartmouth, you can no longer contribute to your HSA account, but you may continue to use the funds in the account.

New Hires will be given the option to enroll in a Health Savings Account in the FlexOnline benefits enrollment system once they enroll in the HDHP with HSA medical insurance option. If you enroll in any other health plan, you will be requried to WAIVE the HSA plan in FlexOnline. If you choose not to contribute your own funds to the HSA account upon hire, you may start, stop or change your annual HSA contribution amount at any time in the FlexOnline system. If you do not elect a contribution amount during the annual open enrollment period, your prior year's contribution amount will not carry forward and you will not have deductions starting in with your first check in January.

Contribution Limits

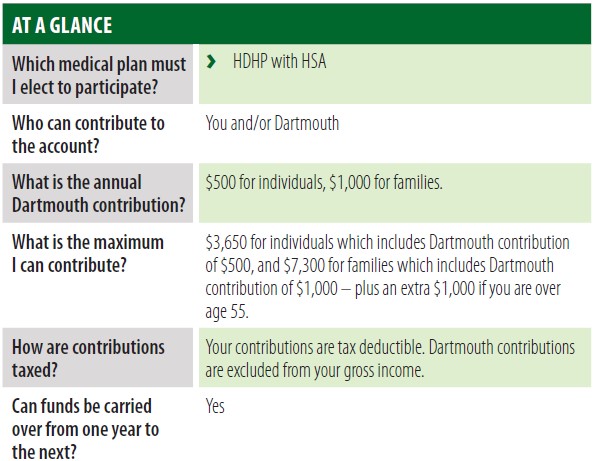

The IRS sets the HSA limits each calendar year. For calendar year 2022, the HSA contribution limits are as follows:

- Individual coverage: $3,850

- Family coverage: (2+): $7,750

- Age 55+ catchup contribution: $1,000

IMPORTANT NOTE: The maximum contribution allowed is determined by the number of months you are enrolled in the medical plan during the year. For example, if you are only enrolled in the medical plan for six months, your annual limit becomes 50% of the amount shown above.

Dartmouth Contribution

When enrolled in the HDHP with HSA medical plan option, Dartmouth will automatically make an annual contribution to your HSA account. The amount is prorated based on your Date of Hire (if new to Dartmouth). Unlike the HCFSA, this amount must be included with the employee contribution when meeting the annual IRS limit.

- Individual coverage: $500

- Family coverage: (2+): $1,000

External Contributions

HSA contributions can be made directly to Fidelity on a post-tax basis and later claimed as pre-tax during your annual tax filing. If you are also making contributions through Dartmouth payroll, please be sure to adjust your Dartmouth contributions accordingly to reflect all external contributions, so as not to exceed the annual IRS limits.

Understanding The Benefit

Health Savings Accounts are strictly regulated by the IRS. It is your responsibility to read and understand the information provided. For clarification about information on this webpage, please reach out to the Dartmouth Benefits office. If you have specific questions around the IRS' rules and regulations surrounding your HSA plan, you are advised to speak to your tax professional.

Fidelity has provided a number of important educational videos to help you get a better understanding of what a Health Savings Account is, how it works and how you can potentially save a lot of money by combining a low cost High Deductible Health Plan with a pre-tax Health Savings Account.

Key Benefits

- The HSA provides a triple tax advantage: money goes in tax-free, grows tax-free, and is tax-free when used to pay for eligible health care expenses.

- You and Dartmouth contribute. You can change your annual contribution amount any time during the plan year.

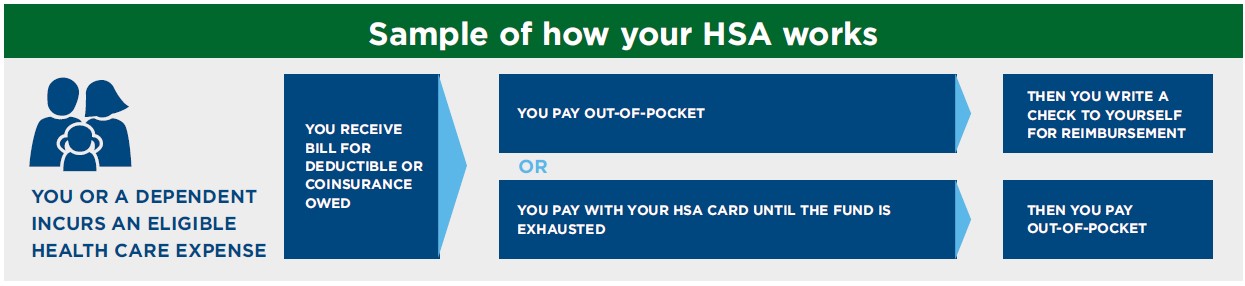

- When you have an eligible expense, you have the option of using a Fidelity provided debit card, checkbook, or you may reimburse yourself through direct deposit.

- Expenses you pay with HSA dollars count toward your annual deductible and out-of-pocket maximums.

- You choose how to invest the money in your account, and your account can grow through investment earnings or interest payments.

- The money is always yours. Besides being free to choose when and how much of your HSA funds to use, any money left over at year's end is yours to keep. You can even take your HSA dollars with you when you leave the plan, change jobs or retire.

- Administration is easy with no stressful submission deadlines.

- The Dartmouth contribution to your HSA account is available with your first paycheck in January and can be used once you have activated your account. Your own contributions are available as they are deposited.

Other Considerations

- Unlike the HRA, payments are not automatic. You decide when and how to use the money in your HSA account. Spend it during the year, save it for the future or open an investment account.

- Consider consulting a tax professional when contributing to a Health Savings Account.

- If you will be Medicare eligible in 2022, please see the HSA & Medicare section below.

*HSA contributions and earnings are not subject to federal taxes and not subject to state taxes in most states. A few states do not allow pre-tax treatment of contributions and earnings. Contact your tax advisor for details on your specific location.

Dependents

While the Affordable Care Act (ACA) allows parents to add their adult children who have not reached age 26 to their health plans, the tax laws regarding HSAs have not changed and children ages 19 until age 26 must be considered a tax dependent in order for an adult child's medical expenses to qualify for payment from a parent's HSA. According to the Internal Revenue Service (IRS) definition, a dependent is a qualifying child (daughter, son, stepchild, sibling or step sibling, or any descendant of these) who meet these three criteria:

- Has the same principal place of abode as the covered employee for more than one-half of the taxable year, and

- Has not provided more than one-half of his or her own support during the taxable year, and

- Is not yet 19 (or, if a student, not yet 24) at the end of the tax year, or is permanently and totally disabled.

One way around this is for an adult child to set up their own HSA. As long as they are covered on the family qualified HDHP, adult children can contribute up to the full family HSA amount into their HSA account. The dependent's contributions will not reduce the amount their parents can deposit into their accounts.

Plan Overview

Refer to page 15 of the 2023 Open Enrollment Guide.

How the Benefit Works

Refer to page 15 of the 2023 Open Enrollment Guide.

Payroll Deduction - Money comes out of your pay check each pay period, and goes into your HSA Account, reducing the amount of taxes you pay each pay period.

Account is Funded - Dartmouth will notify you with instructions on how to set up and claim your HSA account with Fidelity. Dartmouth with load the full employer contribution to your account with your first paycheck in January OR your first paycheck after setting up your account, if you are new to Dartmouth.

Incur Eligible Expenses - If you or an eligible dependent incurs an eligible health care expense that is not covered by your health plan, you then have the option to use HSA dollars to pay for it, or save your funds for future expenses.

List of Eligible Expenses (IRS Publication 502)

Leaving Dartmouth - If you ever leave Dartmouth, or if you change medical plans in the future, this money is always yours and goes with you. You even assign beneficiaries for the funds in the case of your passing. For more information, see the Leaving Dartmouth section at the bottom of this page.

HSA's and Medicare

Per IRS guidelines, you cannot contribute to a Health Savings Account (HSA) if you are enrolled in any part of Medicare or Social Security. Your dependents may be enrolled in Medicare and Social Security, but you as the owner and contributor to the account may not. To avoid a penalty, you should stop contributing to your HSA at least 6 months before you enroll in any part of Medicare or Social Security. The IRS and Medicare do allow you to delay enrolling in Medicare to participate in an HSA, as long as you are still actively working and enrolled in a qualified health insurance plan. Please see the Medicare & You booklet for additional details.

Filing a Claim

Submit/Pay a Claim - If you incur medical expenses and wish to use your HSA funds, then you can use either a Fidelity HSA debit card to pay the provider directly, you can use a Fidelity HSA check book to pay the provider. If you paid the expense out of pocket, you can use the check book to reimburse yourself, or you can set up direct deposit from your netbenefits HSA account and reimburse yourself directly into your bank account. You cannot submit claims for reimbursement that were incurred prior to having the HSA account.

Keep your Receipts - Unlike the HCFSA plan, you do not need to submit your receipts to Fidelity for Substantiation. You will however still need to keep your receipts for all expenses paid from the account, in case you are ever audited by the IRS.

Year End - Unlike the HCFSA, you do not need to spend the full balance in your account by year end. Your full balance, including the Dartmouth contribution is always yours and will carryover from year to year.

Deadlines - The only deadline that you need to be aware of is your tax filing deadline, as you will need to report your contributed balance and balance spent during your annual tax filing.

If you ever forget to pay a bill or reimburse yourself, you can do it at any time. As long as the expense was incurred while the account was active, you can reimburse yourself from your HSA account. Even if it is years later.

Year End Tax Filing

You will be required to report both the amount contributed and/or the amount spent from your HSA account on your annual income tax return each year, regardless of whether you are still enrolled in or are contributing to an HSA account.

- In January, Fidelity will mail form 1099SA to all Health Savings Account (HSA) participants showing the total amount of HSA funds were spent in calendar year 2021. This amount shows on line one of the form as Gross Distributions.

- Box 12c, code W on your 2021 W-2 form will show the total amount of funds that were contributed into your Health Savings Account in 2021. This amount includes both the employer and the employee contribution.

- When filing your taxes, you will need to complete IRS form 8889, using information found on form 1099SA and Box 12W of your 2021 W-2.

- Don't forget to report any contributions that you made directly to Fidelity (outside of payroll deductions).

- Be sure to keep copies of all receipts that support the amount shown in box 1 of 1099SA, in case you are ever audited.

- Always consult a tax professional when you have questions about HSA tax filing and/or eligibility.

Leaving Dartmouth

Your Account - The amount that is in your HSA account when you leave Dartmouth, is your money to keep and take with you. This includes all employer contributions made to date. Your account will remain open and active and you may continue to spend down these funds over time as needed, regardless of the type of health plan you enroll in, in the future.

Packet of Information - Fidelity will not send you a continuation of coverage packet when your benefits end with the college.

Contributions - You may continue to make contributions to your HSA plan as long as you are actively enrolled in a qualified high deductible health plan, whether through your COBRA'd Cigna health plan, the health care exchange or some other qualified HDHP plan.

Contribution Limits - You may continue to contribute up to the IRS' annual limit that you are eligible for.

Administrative Fees - You will be charged a quarterly fee to maintain the account, which will be automatically deducted from your account.

Account Balances - Your unspent balance will continue to roll over from year to year.

Debit Card & Check Book - You may continue to use your HSA debit card and/or check book after you leave the college. Always make sure you keep your receipts for purchases, as you have always done.

Tax Forms - You will continue to receive tax forms at year end and will need to file as part of your annual tax return.

Tax Professionals - When leaving Dartmouth during the middle of a plan year, we highly encourage you to speak to a tax profesional to see how loss of contribution eligibility might impact your annual limit, and how contributions in other tax advantage plans (like HCFSA plans) within the same calendar year could impact your status with the IRS.

Last Updated