Dartmouth College Library Bulletin

The Distribution of Tax-Generated Support for

New Hampshire’s Schoolchildren: 1789-1993

WALTER A. BACKOFEN

New Hampshire made a fresh start on school laws in 1789 by first repealing everything out of its past, which meant chiefly the seminal law of 1647 from the period of Massachusetts governance.[1] The 142 years of unbridled home rule started by that action left New Hampshire’s public school system in a shambles by the time statehood came and a constitution was written to guide future law-making.

Central to the change in 1789 was the rejection of exclusive town-level control over school taxes and the transfer of primary tax authority to the state, but without really doing anything conceptually new. After 1789, school taxes would be raised by exactly the same formula in use since no later than 1693 for paying the bills of the province.[2] Extending this tradition to public schools meant that the General Court would now set an annual threshold of monetary support for all the schools of the state, collectively, and require each town to contribute in proportion to its share of the state’s taxable wealth. A tax was thus imposed by the state, at a nominally uniform rate, to be raised and spent in every town on the operation of its own schools. To spend more was always possible by so voting at town meeting, although an enabling act for that purpose did not appear until 1842.[3]

The mandatory blanket of taxes was increased at irregular intervals during the century ahead, while the assets of the state expanded far more evenly, and after 1900, far more rapidly.[4] Over time, therefore, the nominally uniform and totally derivative state-tax rate cycled more and more widely until finally it required being stabilized by a new law in 1919.[5] But until then, each town’s annual obligatory payment in support of its schools was determined simply and mechanically by multiplying two numbers: one, the total statewide monetary threshold expected to be met by all towns together; the other, the town’s own proportionate share of the valuation of the state. As a practical matter, however, a quill-pen and post-road world did not allow assigning each town its proportionate standing more often than about once every five years, after which it was treated as a constant until the next time around; how that actually worked out is known in unusual detail for the town of Hanover.[6] An inevitable consequence of these stable intervals was an opportunity for the local tax rate to vary from town to town, but probably never by very much before all towns were reapportioned again.[7]

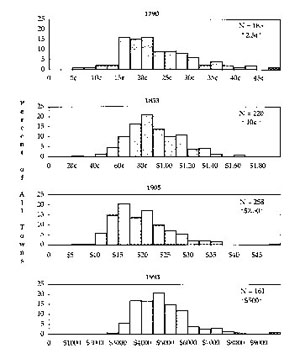

Lists of this town-specific number-called the ‘proportion of public taxes’- were published each time it was determined anew, beginning as early as 1728.[8] This means that the mandatory school tax for any town is easily followed from one level to the next, starting in 1790 when the new law took effect and the two controlling numbers were first multiplied together. Also in 1790, for the first time, a decennial census count of each town’s children, on whom the school taxes were to be spent, becomes available. With those two sets of data-the town’s mandatory payment and the size of its student body-a histogram can be constructed to show how the average amounts required to be spent on schoolchildren compared among all the towns of the state.[9]

As the window opens in 1790, the statewide mandate was �5000, or $16,650[10] from 185 towns or other taxable places. Separating out each one’s obligation and dividing it among its eligible children, to get the average share per child, left 185 different outcomes. And of these, all but the seven largest could be fitted readily into twenty spending slots, each 2.5� wide, for a support-payment distribution well skewed toward the high end in the topmost histogram in Figure 1. Cutting off the distribution at 50� in 1790 facilitates the comparison with future histograms. But even doing that leaves a support-payment range spread out by about a factor of eight; and when those omitted are brought back in-mostly from Grafton County settlements so small that under the old law of 1647 they would have been excused from having to teach their children to read and write-the spread-ratio goes up to nearly twenty to one: From Dame’s Location with sixteen eligible youngsters and only a little more than 5� for each, at the far left, the upper limit actually topped out in Dalton with $1.00 for each of eight children in need of schooling, well out of sight at the far right. Among long-established settlements in Rockingham County in 1790, the averages were 9.3� apiece for Newcastle’s 234 scholars and 58� for South Hampton’s 162, for a difference, in this case, of a little more than a factor of six. The state-wide average was almost 25� per child (from $16,650 and not quite 70,000 eligible students), while towns or places spending between 15� and 22.5� represented nearly half of all the state’s settlements in what might be read in Figure 1 as a modal frequency of around 17%. The payment tail reaching up-the-scale so far in 1790 never fully disappeared as long as a few towns spent at far above average rates. But the vestige of that tail in later times was no longer this early catch-all for precarious northern outposts with few children, although occasionally with almost as many dollars for their education.

The next histogram down in Figure 1, identified as from 1833, combines the school taxes newly mandated for each town in 1833 with children from the census of 1830; the distribution, in the same number of intervals used in 1790 but each now widened from 2.5� to 10�, has gotten to look almost normal. After forty or more years, 22% of all towns, in a well-defined mode, were supporting their schoolchildren with an average outlay of between $0.80-0.90 apiece. Ending the payment range at $2.00 per scholar leaves out only four places in 1833, all in Coos County, where school-tax revenues of $8-$11 distributed among one to five scholars led to per capita allotments of $2.55 to $8.10, with the highest for Dixville’s single scholar. Those aberrations aside, it is more significant to compare Hampton Falls, with its 181 scholars enjoying the highest unit spending rate of $1.62, and Effingham, with 733 scholars and almost the lowest rate of $0.41 (a nearly four-to-one difference); only Hale’s Location, also in Coos County, raised as little as $0.26 apiece for its fourteen scholars, which meant a better than six-to-one difference compared to Hampton Falls, although if Hale’s Location is matched with Dixville, the comparison goes up to more than thirty-to-one. Meanwhile, Franconia, Stratford, and Newcastle spent about the same $1.40-1.45 per scholar for head counts of 151, 171, and 288, respectively. As a statewide average, the outlay per scholar rose to virtually $1.00, or about 10% more than the mode.

Fig. 1. Average child-support payment by town; N = number of towns.

Nathaniel Bouton, the historian of Concord, New Hampshire, in 1833 lauded what he saw to be the state’s generous and equitable support for public education in this year of the histogram, especially singling out the $90,000 statewide mandate and its translation into almost $1.00 for each student in the system.[11] That his average came from a support distribution spread out over a range of 30 to 1 drew no comment from him. Nor did it draw one from New Hampshire’s present Supreme Court when it made Bouton’s upbeat commentary on early education its first New Hampshire citation in the proof-of-adequacy argument behind the so-called Claremont-I decision.[12] But if Bouton’s $1.00 average was also what he knew the actual average to be, an interpretation of the $0.25 from 1790 as another real average is bolstered. In that case, the ratio of the two statewide averages from 1833 and 1790�$1.00/$0.25 = 4.00-would mean that the support rate had advanced only according to the legislature’s design, i.e., $90,000/$16,650 = 5.4 from mandate growth was diluted by a factor of 96,000/70,000 = 1.37 from growth in the eligible student population, to leave a net gain of 5.4/1.37 = 4.00. This is equivalent to reading the two histograms for these years as spending scenarios from a time when there was no serious voluntary overpayment, and all school taxes reflected essentially the same mandatory rate for every taxpayer each year. Other evidence that this was probably not far from the truth can be found in a review of the balance sheets published by the state for all towns after 1850,[13] which comes under scrutiny, later, in Figure 2.

To pursue the town-by-town funding analysis after 1840 would generally require consulting the manuscript census for the student populations of all small towns. But fortunately, the makings of another statewide support distribution show up in the biennial report of the State Board of Education for 1905-1906, where the average outlays per student are listed for all towns in the state in 1905.[14] From these came the third histogram in the series, showing how payments compared after the statewide average had climbed to within a few cents of $20.00 per child. The distribution remains fairly normal-looking in intervals now grown to $2.50, with the same modal frequency as in 1833, at 22%, and limits about as far apart, proportionately, as they were seventy years earlier. At the same time, the state’s mandatory revenue-threshold was raised to $750,000 in 1905, the highest it would ever get to be under the formula of 1789, and larger by a factor of 8.33 than it was in 1833, at $90,000. Along the way, however, the student population declined from 96,000 to about 65,000 (a little less than it was in 1790), or by roughly 30%, which effectively inflated this gain to something more like 8.33/0.70 = 12 on a per capita basis. Still, there was almost twice as much growth in the statewide average support, as it climbed from $1.00 to $20.00 per capita between 1833 and 1905. Collective overspending across the state in 1905 thus boiled down to the difference between ($20.00/head � 65,000) = $1,300,000 and $750,000, or better than 70% of that year’s mandate. Subtleties of numerical comparison aside, the significant conclusion is that by 1905 the state, through its legislature, was no longer the sole driving force behind revenue generation for public schooling. Almost as much revenue was now coming from the voluntary decisions of taxpayers spending, in the aggregate, well above mandate levels.[15] But with over-spending decisions voluntary by town, there was little that was systematic about the response.

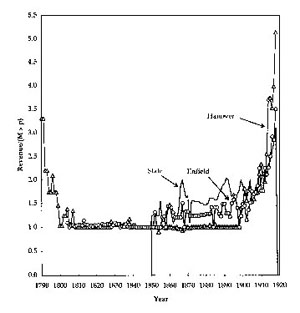

Fig. 2. Total school-tax revenue after dividing each year's by the town's mandated payment of M x p, to show proportional excess. The Enfield record does not begin until 1804. Mandated revenue for the state, known each year, was M x 1000; actual revenue was not recorded until 1850. (See Note 9 for review of terminology.)

A good example of how this turned out locally can be found in well-preserved evidence from the neighboring towns of Hanover and Enfield. The Hanover analysis appeared earlier in the this journal.[16] Enfield has since come under the glass.[17] Both sets of results are compared in Figure 2 using the earlier gauge of overpayment, namely, the ratio of all money actually spent on a town’s schools to the corresponding sum mandated by the state. Without overpayment the ratio is unity, so that any amount beyond 1 is the overspending proportion. The comparison cannot begin until Enfield first goes on record in 1804, but after that neither town shows any significant advance beyond its state-decreed threshold for almost the next half century. Then, in 1852, Enfield abruptly set out on something of a saw-tooth path of overspending by 25-50% per year, which lasted for about fifty more years. Hanover, meanwhile, carried on as before until nearly the end of the century when it finally joined in, and overspending in both towns accelerated. By now, the state, as a whole, was almost 100% above its mandate on a spending schedule that cannot be discovered until 1850.[18] But from that year on, the irregularly-climbing upper edge of the shaded region in Figure 2 represents the combined excess in taxes paid at the town and district levels everywhere, relative to the statewide mandate base. Extra-mandate growth across the state thus developed over time from a weak beginning, suffering assorted reverses in the process-some brought on by national panics and depressions-as well as getting recharged for a few years with the abolition of the multidistrict school system in 1885. Before the enduring influence of the law of 1789 ended in 1919, Hanover did, finally, pull well ahead of a pack that was also accelerating by then, although far from uniformly.[19]

To complete the scan in Figure 1 with a present-day anchor, the fourth histo-gram, for 1993 and in $500 intervals, has been based on the historically important data from the time of the Claremont-I decision.[20] Such widespread support dis-parities in 1993 were broadly viewed as evidence that the present system was failing to meet the obligation that the Court found to be implicit in the Constitution: an adequate education, adequately funded. Yet despite radically different tax laws dating back to 1919,[21] the latest support distribution does not look much different from earlier periods, except for scale factors. The frequency of the most common payment-close to $5000.00-is the same as it was in 1905 and 1833, although the full range of payments, that reached out to 20-30 to 1 in earlier days, is down to only about 4 to 1 in 1993.

Even a support disparity of twenty- to thirtyfold could easily have understated the problem facing some schoolchildren during the district-school era of 1805-1885.[22] For then, the average town was subdivided into a dozen or so practically independent academic fiefdoms. And however support differed among those districts, it never showed up in the townwide average, which was all that could be found for the histograms. The ultimate difference, of course, would have been met in the district too poor or parsimonious to offer any school, as sometimes happened before 1885.[23]

By far the greatest single change over this span of 203 years came about in the average yearly unit expenditure at the state level. That grew by about a factor of 20,000 between 1790 and 1993, in the same period that saw the cost of the average childbirth without complications increase by a factor perhaps only one-tenth that large. Tax strategies, cultural priorities, and amounts of money raised, more than the intertown range in support of schoolchildren, differentiate the two ends of the histogram display.

In effect, a more or less normal distribution moved upscale in Figure 1 at a growsing speed as the clock ticked, gaining about ten times as much ground in the last interval (1905-1993) as in the one before (1833-1905), with only about 20% more time. Before that, growth in the second interval was five times greater than in the first (1790-1833) with less than 70% more clock time. Given the uncertainty about statewide overspending before 1850, a growth comparison from both sides of this bookkeeping divide must err on the side of exaggeration. But given also that overspending was essentially on the rise as it came into view in 1850, it was probably lower once, while looking backward on the straight path made by filling the early valleys with the peaks in the statewide overspending profile (Figure 2) does seem to locate its beginning somewhere after the first of the century. Thus, even if actual spending in 1833 was increased by 20%, say, the outcome at this level of discussion would hardly be changed.

Equity for schoolchildren, which intuitively calls for a narrowing of the distri-bution, has apparently never caught up with cost, not even as inequity in virtually mandatory tax rates to meet those costs was to become a dominant part of school-support policy. With the focus today on adequacy more than equity, future support distributions are likely to continue being spread out, as the adequate-for-what-purpose issue is resolved. But if adequacy was always New Hampshire’s intent, and must now be restored, the challenge is to decide when that intent was abandoned.

[1] Massachusetts, Records of the Governor and Company of the Massachusetts Bay in New England, Printed by order of the legislature, 5 vols., ed. Nathaniel B. Shurtleff (Boston: W. White, 1853-1854), 2:203. For a more extended discussion, see Walter A. Backofen, New Hampshire’s Public School System: 1789-1919: The Taxpayer-Oriented Years (E. Plainfield, N.H.: Lord Timothy Dexter Press, 1994).

[2] New Hampshire, Laws, Statutes, etc., Laws of New Hampshire: Including Public and Private Acts and Resolves and the Royal Commissions and Instructions, with Historical and Descriptive Notes, and an Appendix, ed. Albert Stillman Batchellor, 10 vols. (Manchester, N.H.: J. B. Clarke, 1904-1922), vol. 5, First Constitutional Period 1784-1792, 449-450.

[3] ‘Of Assessment and Apportionment of the School Tax,’ New Hampshire, Laws, Statutes, etc., The Revised Statutes of the State of New Hampshire, 1842, Chap. 72.

[4] W. A. Backofen, ‘A Quintessential New Hampshire Policy: The Seemingly Forgotten Mandatory School Tax of 1789 to 1919,’ Dartmouth College Library Bulletin, n.s., 40:1 (November 1999), 21-29.

[5] ‘An Act in Amendment of the Laws Relating to the Public Schools and Establishing a State Board of Education,’ New Hampshire, Laws, Statutes, etc., Laws of the State of New Hampshire (1919), Chap. 106.

[6] Walter A. Backofen, ‘The Town of Hanover as a Window on Public-School Funding in the State of New Hampshire: 1789-1919,’ Dartmouth College Library Bulletin, n.s., 39:1 (November 1998), 26-43.

[7] Backofen, ‘A Quintessential New Hampshire Policy.’ See also Walter A. Backofen, ‘New Hampshire’s Proportion of Public Taxes: Its Role in Public School Funding: 1789-1919,’ Dartmouth College Library Bulletin, n.s., 34:1 (November 1993), 17-24, for a discussion of the state-tax policy that lasted until 1939.

[8] Backofen, ‘New Hampshire’s Proportion.’

[9] In the terminology introduced in Note 7 and applied in Note 6, the mandatory annual school tax for any town was M x p, where M was the multiple of $1000 demanded from the state overall, and p was the town’s dollar obligation for each $1000. Dividing M x p for 1790 by a corresponding tally of eligible scholars in New Hampshire, from the federal census of 1790 (United States, Census Office, Return of the Whole Number of Persons within the Several Districts of the United States (Philadelphia: Printed by Childs and Swaine, [1791])), yields an average per capita outlay that serves well to anchor the opening year. To get the tally of scholars in 1790 also required some interpretation of the enumerators’ data, which provided only the ‘number of free white males under 16’ as a relevant cohort. But because gender discrimination in public schools was never intended, the available cohort was simply doubled to discover a total for both sexes. And although that block was too young overall, it most probably contained about as many as in the same number of age levels more appropriate for school attendance, i.e., 4 to 19 instead of 0 to 15. The exercise was more straightforward in 1833 when each town’s mandatory school tax was divided by all of its 5- to 19-year-olds as separately tabulated in the census of 1830. The historian Nathaniel Bouton remarked that the intent was for public schools to be open to all aged four through twenty, to make the accessible cohort only about 10% less than Bouton’s ideal; see his The History of Education in New Hampshire, A Discourse Delivered Before the New Hampshire Historical Society (Concord, N.H.: March, Capen and Lyon, 1833).

[10] An equivalence of 3.33 U. S. dollars to 1 U. S. pound was recognized until well into the nineteenth century. An early tabulation of exchange rates, which may be the first reference to make this clear, is ‘Tables, shewing in three different view [sic] the comparative value of the currency, of the states of New-Hampshire, Massachusetts, Rhode-Island, Connecticut, Virginia, Vermont and Kentucky, [microform] : with dollars, cents and mills, and sterling money; : also, of French crowns, with dollars, cents and mills, and with currency, and of foreign coined gold, with dollars, cents & mills,’ Early American Imprints, First Series, no. 31266 (Portsmouth, N.H. : Printed by Charles Peirce, proprietor of the work), 1796. In 1790, New Hampshire’s blanket school-support threshold was set at �5000. Here, that sum has been converted to $16,650 using the 3.33-to-1 equivalence. After 1794, all such thresholds were framed in dollars, directly.

[11] Bouton, History of Education.

[12] New Hampshire, Supreme Court, The New Hampshire Reports 138 (1993-1994), 183-193.

[13] Backofen, New Hampshire’s Public School System, 42 ff.

[14] New Hampshire, State Board of Education, Biennial Report of the New Hampshire State Board of Education (1905-1906), Appendix E, 421-426.

[15] Backofen, New Hampshire’s Public School System, 44.

[16] Backofen, ‘The Town of Hanover.’

[17] Details can be found in a working draft of the author’s ‘The Public School System in Enfield, New Hampshire: 1789-1918,’ the tentative second chapter in a forthcoming monograph on the history of Enfield’s children, at work and in school.

[18] Backofen, New Hampshire’s Public School System.

[19] An interesting correlation with the post-1905 spending upsurge is the end of state-mandated funding increases in that very year. Perhaps the outburst of aggregate voluntarism, although based on a rapidly depreciating dollar, made the funding managers indifferent to trying to drive spending any faster, even though there were always towns that fell through the cracks.

[20] New Hampshire Reports 138 N.H. 183.

[21] ‘An Act in Amendment.’

[22] The multidistrict plan was born in 1805 with ‘An Act Empowering School-Districts to Build and Repair School Houses, and Regulating Schools,’ New Hampshire, Laws, Statutes, etc., Laws of New Hampshire: Including Public and Private Acts and Resolves and the Royal Commissions and Instructions, with Historical and Descriptive Notes, and an Appendix, ed. Albert Stillman Batchellor, 10 vols. (Manchester, N.H.: J. B. Clarke, 1904-1922), Vol. 7, Second Constitutional Period, 467-469. It ended with ‘An Act in Amendment of Chapter 86 of the General Laws, Relating to Schools, and to Establish the Town System of Schools,’ Laws of the State of New Hampshire (1885), Chap. 43.

[23] A discussion of this point can be found in Backofen, New Hampshire’s Public School System.